Vietnam’s tightening credit market has impacted SMEs and corporates from various industries. While the market has been experiencing a significant funding shortage, the government has been taking action to destress the economy and keep businesses moving.

Recently, Prime Minister Pham Minh Chinh went on record instructing the banking system, specifically the central bank (SBV), to act quickly in freeing up credit. If they cannot, the effect on local businesses and general market sentiment could be severe.

Highlights of this article

- Inflation Tightens Monetary Situation The sustainability and liquidity trade-off by policymakers

- Construction, Manufacturing and Banking Sectors Hit the Hardest Banks go from facing a liquidity squeeze to having cash surplus

- A Positive Future Outlook Stabilising market with actionable government measures to drive GDP Growth

- How Can Velotrade’s Financing Solutions Help? Supporting businesses during both good and tough market situations

Why is Vietnam Facing a Credit Crunch?

Vietnam’s credit crunch is the result of various factors, including:

- the tight monetary situation caused by rising inflation

- excessive lending by banks in the first half of 2022

- limited credit room growth due to policymakers’ focus to control inflation

While these factors have contributed to the credit crunch, policymakers believe it is essential to maintain a balance between controlling inflation and sustaining the banking industry in the long run.

To truly understand why Vietnam is facing a credit crunch, let’s delve deeper into the factors affecting the country’s monetary policy and banking industry.

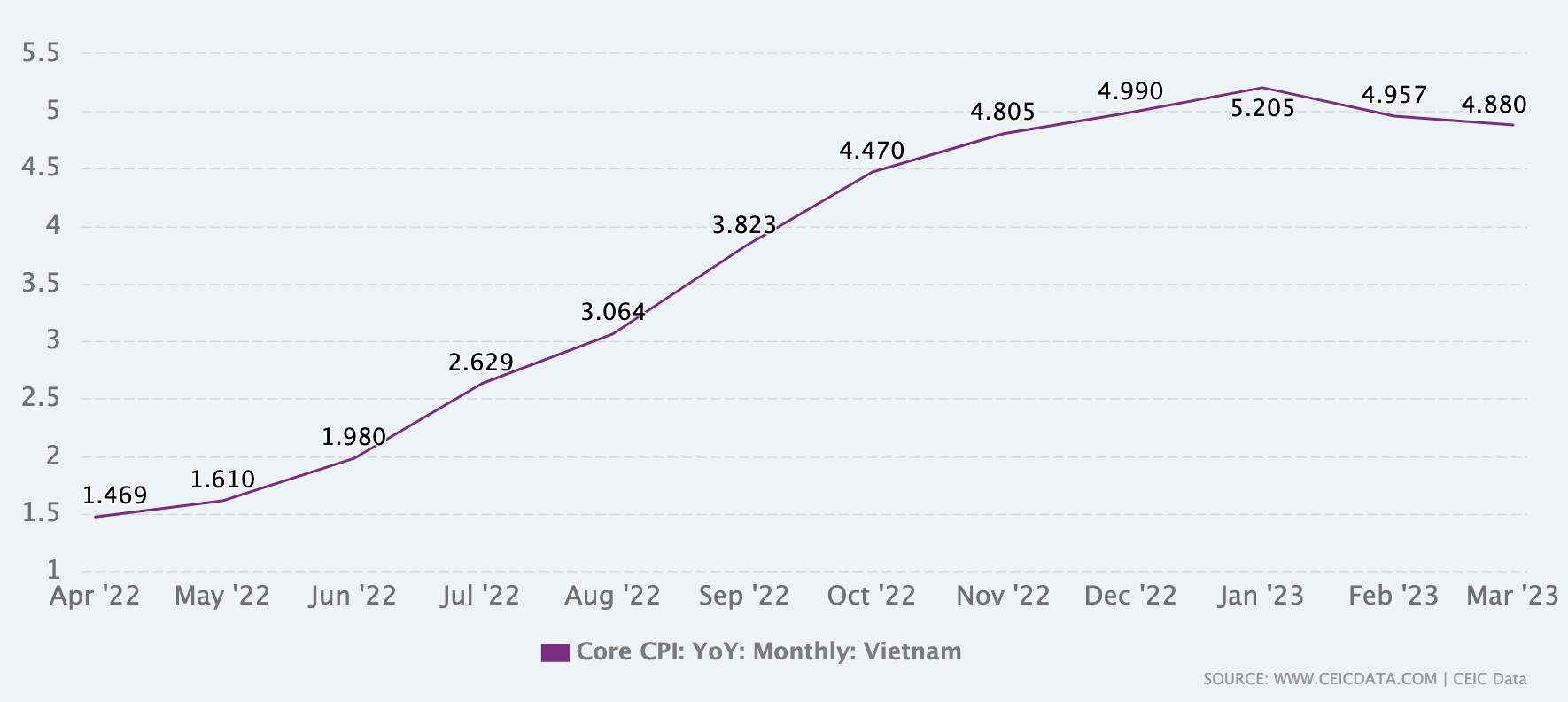

With inflation rising persistently since September last year, Vietnam seems to have reached its peak at 5.2% in January this year.

Vietnam’s Monthly CPI rate, CEIC Data, 2022-2023

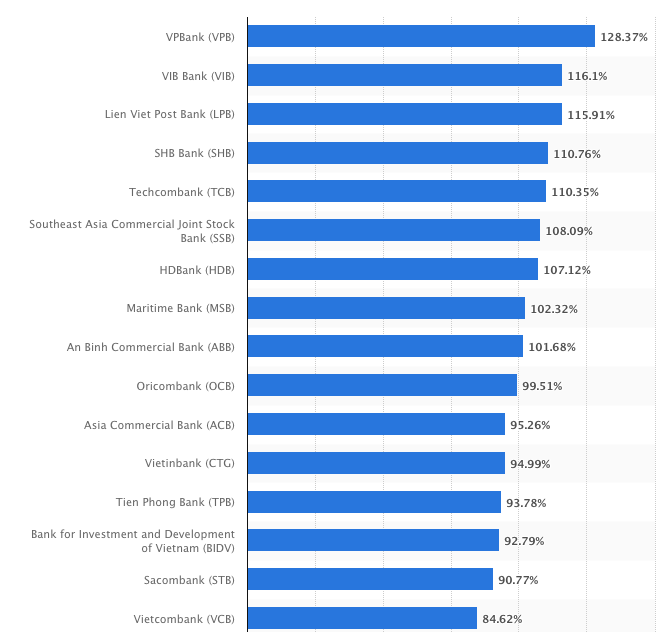

This has caused banks to set high lending and deposit rates to attract more capital. However, slower deposit growth relative to credit has led businesses to invest more in the stock and bond market.

Moreover, banks require higher deposits to lend more, but lower deposit rates have prevented this due to a high loan-deposit ratio among major banks shown in the figure below.

Loan-Deposit Ratio of Vietnamese Banks, Statista

Although credit limits started to increase after the pandemic, deposit growth was still much slower than credit growth.

In response to the credit shortfalls, the State Bank of Vietnam provided an additional credit of around 200,000 billion dongs. However, this increase in credit room was insufficient and did not have the impact that was promised. The extra liquidity was only granted to 15 out of the 35+ banks in Vietnam that are financially healthy and met the required qualifications. The bank’s stringent approach did not have the desired impact.

From the banks’ perspective, the growth in credit room has been much higher than the credit limit, leaving them with little source of capital to provide lending. The small loosening of credit has mostly been sufficient to fulfil existing loans, not extend new ones. Priority areas and businesses, as per the government policy, must be targeted first, leaving many businesses out.

On the contrary, the policymakers’ goal is to control inflation, and expanding credit limits can cause inflation to get out of control. Hence, limited credit room growth is necessary for long-term sustainability in tight market conditions.

![]()

- Excessive Lending in the First Half of 2022 Causes a Liquidity Squeeze This caused banks to set high lending and deposit rates to attract more capital.

- Credit Growth Has Been Slower than Banks’ Credit Quota The additional credit lending by SBV to fill capital scarcity was insufficient to meet the high loan demands of all businesses.

Impact of Credit Crunch on the Vietnam Market

Vietnam’s tight economic situation has impacted various sectors significantly. The real estate and construction industries, particularly, have been hit hard, while larger industrial companies continue to have credit access at higher interest rates.

Real estate developers and smaller companies have primarily been affected, as local banks have become more selective in their lending. This has caused developers to face an Asset Liability Mismatch problem as they need to repay their outstanding debts every two years. Yet, the raw land they purchased will not generate cash flows until well into the future.

To fund their land banking, developers have turned to the corporate bond market, which has grown significantly in recent years. However, with $12.8 billion of corporate bonds maturing this year, many issuers have an urgent need to refinance or extend bond maturities to avoid defaults.

This lack of funding has also led property developers to delay new projects, which has caused a slowdown in the construction industry. This slowdown in construction has also affected the manufacturing industry, as construction is a significant driver of demand for industrial goods.

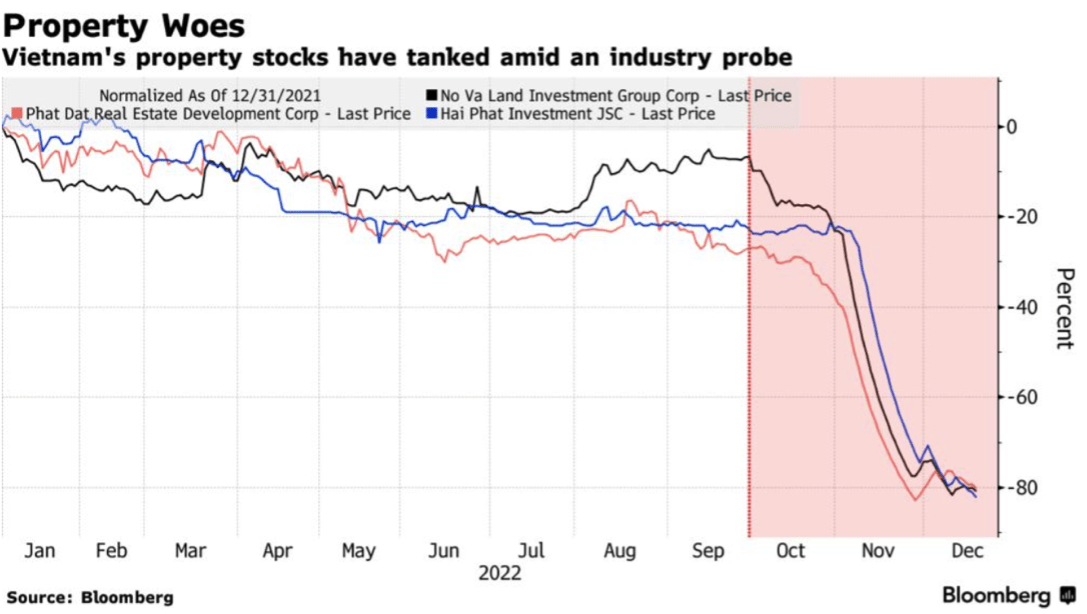

NoVaLand Investment Group Corp. and Phat Dat Real Estate Development Corp. have both seen their shares go limit down for at least 17 straight days.

Vietnamese Property Stock Prices, Bloomberg, 2022

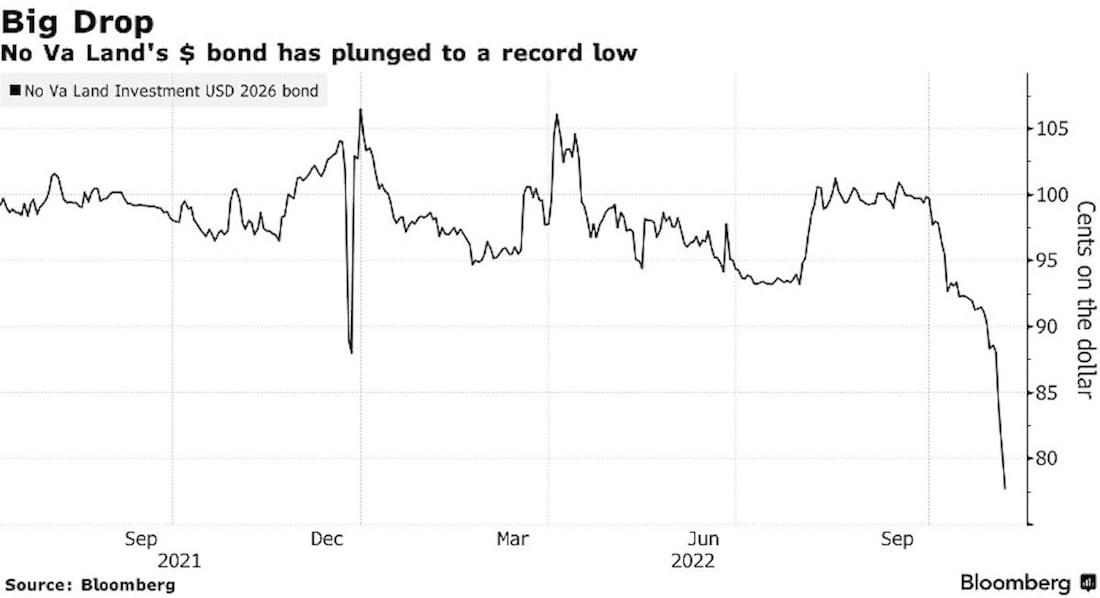

NoVaLand’s 2026-dollar bond also plunged to a record low. The situation occurred due to a corruption probe that hit the country’s property developers, pummelling domestic debt sales.

No Va Land Bond Price, 2021-2022, Bloomberg

This turned the local stocks into the world’s worst-performing benchmark. Besides, Vietnam’s finance minister’s pledge to ease funding woes for builders has not been enough to calm investor concerns.

This liquidity squeeze has also impacted the banking sector. Banks were initially more risk-averse and selective in their lending due to the high credit demand and capital shortage last year. However, growing international and domestic market uncertainties have adversely impacted firms, especially SMEs, making it difficult for them to meet banks’ lending conditions. This has slowed credit growth in the first quarter of 2023 drastically, causing banks to have excess liquidity that resulted in lower overnight interbank interest rates.

![]()

- Real Estate and Banking Sectors Suffer the Most Developers face difficulties in meeting debts, while banks become more selective in their lending.

- Decline in Deposit Demands Create Excess Liquidity for Banks While GDP growth is resuming in Q1 2023, businesses have become more risk-averse in their capital-sourcing options.

Recent Changes in Market Dynamics

Despite all the hardships, Vietnam’s economy has shown some resilience and is expected to resume growth as global manufacturing supply chains shift to Southeast Asian manufacturing hubs.

Vietnam’s banking system has a money surplus as banks do not require capital from the State Bank of Vietnam’s open market operation channel (OMO), causing a sharp drop in overnight interbank interest rates. The country’s central bank has pledged to keep monetary policy flexible and inflation below 4.5% for the rest of the year to meet the target of 5.5% real GDP growth.

To control inflation and recover production levels, the SBV announced the following on 23 May 2023:

- a lower open market operation (OMO) interest rate from 6% to 5.5%

- a cap on the VND deposit interest rate for organisations and individuals on short-term deposits

The purpose of both measures is to reduce the lending rate and stimulate economic growth by allowing businesses to access credit at cheaper rates. This will play a vital role in easing the tight credit market situation facing businesses in Vietnam.

Analysts also see easing bond rules as a potential pressure release valve, as Decree 65 pummelled property stocks and chilled new bond issuance by raising the bar on disclosure requirements as well as limiting the type of buyer to institutional investors only.

Any improvement in the nation’s property market will require major amendments to Decree 65, according to Maybank analyst Tyler Manh Dung Nguyen, who predicts the government is likely to respond when it sees the next round of developers’ corporate earnings next year.

The government has already appeared to ease its stance, with the issuance of new Decree 08 in March 2023 allowing companies to extend corporate bond maturities up to two years to ease funding shortages.

Vietnam’s leaders remain focused on the nation’s economic growth targets as it seeks to become a major manufacturing hub. Having already attracted the likes of Apple Inc. suppliers and Samsung Electronics Co, Vietnam’s growing technology sector is playing a pivotal role in this shift. Technology advancements are expected to bring about a 1.1% annual increase in GDP growth for Vietnam. The country is willing to move quickly and proactively to address risks.

Finance Minister Ho Duc Phoc said last month that the government is taking measures to ease capital access for developers given the rout. However, more needs to be done to lure investors back into the bond market.

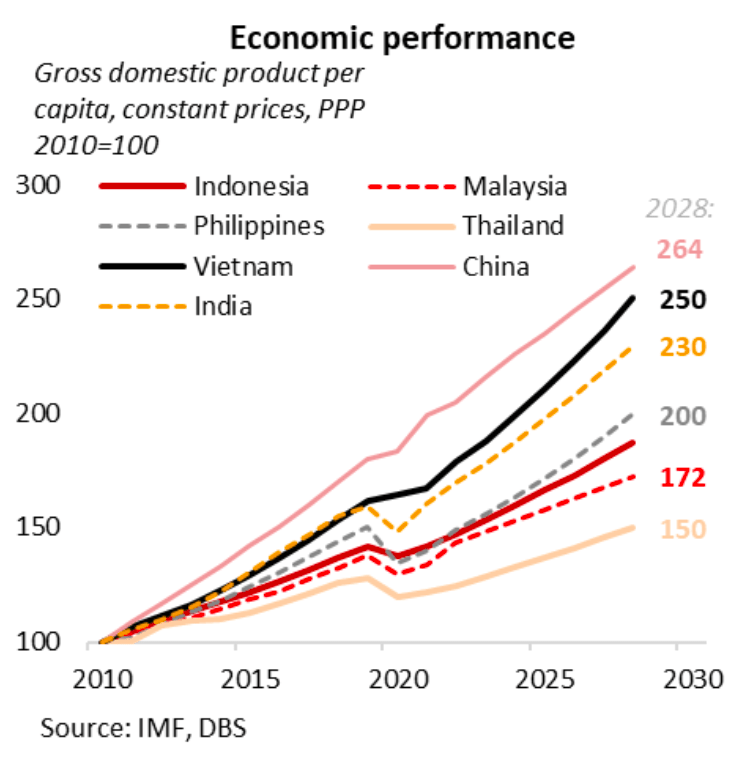

In light of all this struggle, Vietnam’s GDP is still expected to grow, while corporate earnings are on track to increase by 17%.

GDP Growth Projection, DBS Research, 2010-2030

While the country’s FDI and export-oriented model is contributing to this robust growth, the central bank’s pressure to abide by the government’s anti-dollarisation policy is limiting trading opportunities for foreign businesses. Although the 0% return on USD deposits is helping the country in reducing foreign currency mobilisation and maintaining exchange rate stability, smaller importers and exporters are being left without credit lines in USD.

An increasing number of foreign businesses are being impacted as banks become more selective in their lending. This is where alternative financing solutions can help!

![]()

- Bond Market Eases with Vietnam’s New Decree 65 Regulation Vietnam’s finance ministry proposes to extend corporate bond maturities to 2 years to ease funding shortages.

- The Future is Bright for Vietnam The country’s strong technological capabilities and export market is making it an attractive manufacturing hub for foreign businesses.

How Can Alternative Finance Help?

Alternative financing can be a vital source of growth in both good and bad economic times for businesses.

While Vietnam’s tight credit market may be easing, there are still businesses struggling to make ends meet. Low-priority businesses and SMEs particularly face difficulties accessing credit and fail to meet banks’ high lending requirements.

Alternative financing solutions can help fill this funding gap left by banks and other traditional lenders. With greater flexibility and customisation options, businesses can get tailored funding solutions that best fit their specific needs and growth plans.

Meanwhile, during times of economic growth, growing businesses can diversify their source of capital to further stimulate growth and drive innovation. Traditional financial institutions may be unable to meet such businesses’ credit requirements. This is where alternative financing companies like Velotrade can provide the extra capital to fund these businesses’ growth at a much faster pace.

Having been serving the Vietnam market since 2018, Velotrade can be a reliable financial partner to support your domestic and global trades due to several reasons:

- Having financed hundreds of Vietnamese businesses, our Vietnam sales team have the expertise to deal with businesses of different natures with a sound understanding of the local culture and requirements.

- From wholesale, retail, and furniture to manufacturing, we have experience financing a wide range of industries and understand the challenges faced by each.

- Our Vietnam team of experts are well-versed in local lending regulations and standards with a solid risk assessment structure in place.

- Vietnamese importers or exporters trading with foreign businesses in need of foreign capital (like USD) can meet this cash shortfall that local banks are unable to provide due to government and policy limitations. Meanwhile, domestic traders that are unable to get support from banks can continue and grow their business productions with Velotrade’s digital financing solutions.

Wait no more! Whether you are a business based in Vietnam or exporting to the country, connect with us and our local or international sales experts will support you at their best.

Brought to you by Velotrade, a marketplace for corporates to access financing.

About the author

Velotrade Editorial

Official content from the Velotrade team.