Asset financing lets a business borrow money to purchase assets, while asset-based lending is when a company borrows money and uses what it already owns to guarantee payment.

Both facilities help businesses expand and grow in operations, allowing them to increase their production capabilities. With more machinery and funds to support the business, companies can attain higher sales.

Let’s unwind the difference between these 2 types of asset finance in greater detail.

Highlights of this article

- 2 Types of Asset Finance Know the 2 ways to attain assets using financing

- 3 Types of Asset-Based Lending Understand how and why each type can be used as collateral

- Which Solution Works Better? Discover why you should or should not choose asset finance and asset-based lending depending on your needs

What is Asset Finance?

Asset finance is how businesses borrow money to purchase or rent an asset for business operation and growth.

An asset is a resource or property owned by a person or a company that creates a positive economic value. It could be buildings, offices, vehicles, IT software, and equipment.

Banks or financial intermediaries usually provide asset finance services. Like a regular loan, the client repays the original asset value plus the fees to the asset finance company for repayment.

The terms and conditions usually vary greatly depending on both parties.

Types of Asset Finance

There are different ways to attain assets with financing, which can be confusing due to their high similarities. Here are 2 key ways:

Hire Purchase

This involves purchasing an asset (usually expensive) where the business pays the asset value in instalments with interest over an agreed period.

It usually requires an initial down payment, and once all instalments are made, the lessee owns the asset.

Leasing

Another approach is to rent the asset for the period required. There are two main kinds of leasing:

- Finance (Capital) Lease - where the borrower attains asset ownership by the end of the lease term

- Operating Lease - where the ownership right remains with the lender

Leasing allows businesses to use assets that they otherwise couldn’t afford.

What is Asset-Based Lending?

Asset-based lending is the practice of loaning money secured by assets already owned.

Asset-based lending includes liquid and illiquid assets from the balance sheet, such as properties, machinery, and unpaid invoices (also known as accounts receivables).

Types of Asset-Based Lending

Let’s delve into some of these commonly used assets as collateral to access financing:

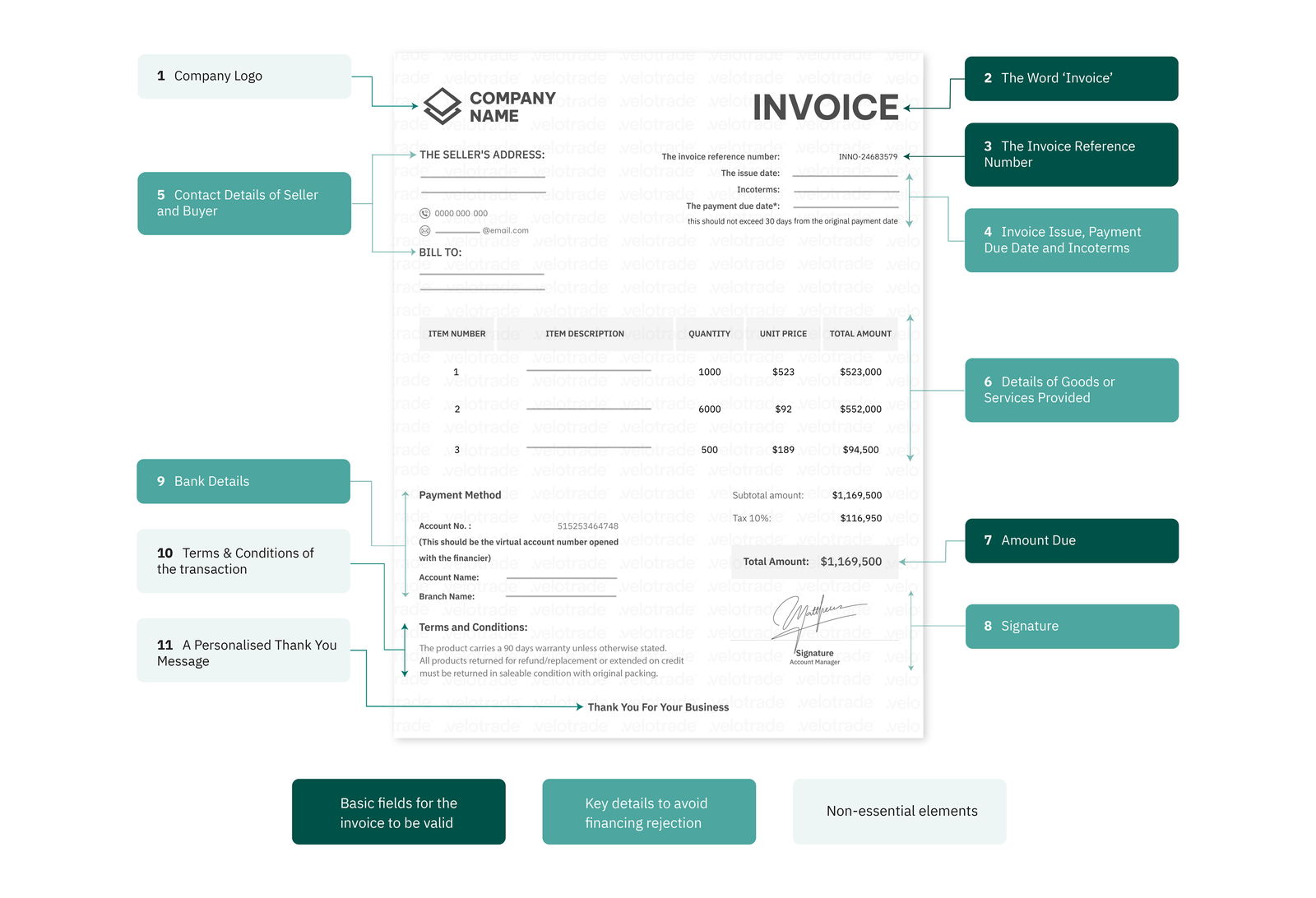

Invoice Financing

Businesses can get early access to cash trapped in invoices and receivables owed by customers through different invoice-based lending.

Invoice discounting is one of the most common and fastest means to access capital due to its short tenure.

This is where financing is backed by receivables which are unpaid invoices that serve as collateral assets.

Find out how invoice discounting helps a business ramp up its operations.

Factoring an invoice is another alternative used by companies where the invoice is sold to a factoring house. In this scenario the credit management process is outsourced.

Brought to you by Velotrade, a marketplace for corporates to access financing.

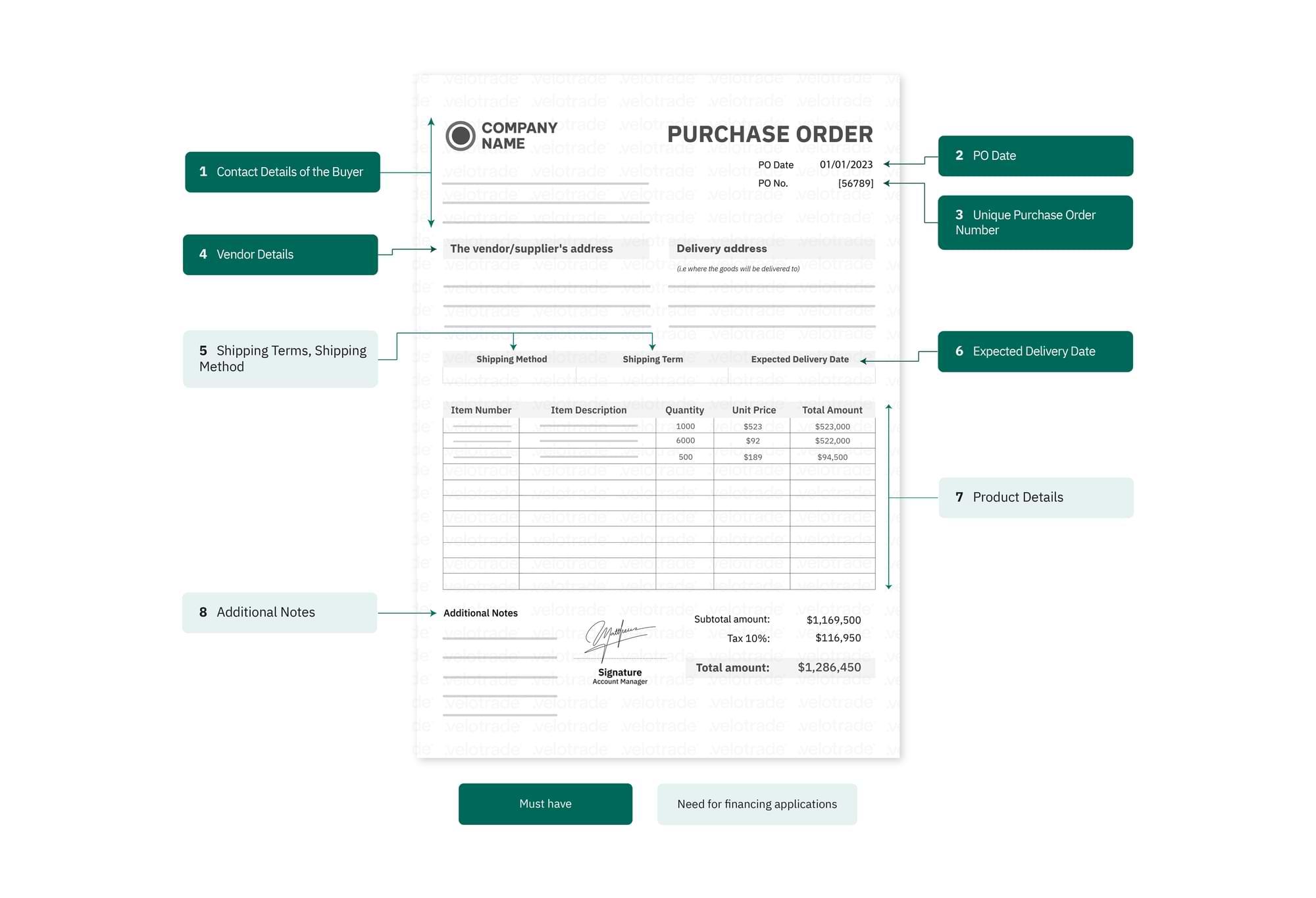

How can firms access Invoice Financing solutions?

Unlock the steps of the invoice financing process and understand the role of the different parties involved.

Equipment Financing Businesses can also pledge their equipment as collateral to secure funds. In this case, the loan amount is based on the equipment value. Factors like the time value and condition of the equipment determine the loan amount. If the loan fails to repay, the lender recoups the equipment used as collateral.

Real Estate Financing Properties are also a common type of asset used to secure capital. Loans backed by mortgages are secured loans as real estate tends to retain value over time. The high value of properties allows businesses to secure more funding.

![]()

- Both Facilities Support Business Growth While asset finance helps businesses achieve more with new capital acquisition, asset-based lending makes existing business operations more efficient.

- Securing Assets Through Financing Businesses can choose to own or rent the asset used as collateral. The latter can be more expensive due to the high instalments for every new rental.

- **Securing Financing Through Assets **Invoice financing is a less risky collateral option where the business does not have much to lose as no personal assets are put to stake.

Why Use Asset Finance and Asset-Based Lending?

The benefits are abundant regardless of whether you use financing to purchase assets or use assets (as collateral) to obtain funding.

It all depends on the growing needs of the business.

- Securing Assets Through Financing

Minimal Upfront Costs:

Assets are vital to a company’s operation. However, many of them tend to be quite expensive, especially for SMEs who are tight on budget.

Asset finance helps businesses pay minimal upfront costs.

Releases Working Capital:

Businesses can free up working capital as the asset’s cost can be spread over time: repayments are made in instalments along with interest.

Crucial capital to be spent on the asset can thus be invested in business expansion activities.

Decreased Risk for Seller:

Upon leasing, the asset provider takes the risk of depreciation, asset servicing, and replacement until the client has made the full payment.

- Securing Financing Through Assets

Objective Valuation Based on Asset:

Using assets as collateral allows businesses to get financing based on the asset value, not just a company’s creditworthiness.

Collateral-Free:

Businesses can get quick access to capital using receivables as collateral. No additional assets are required to support the financing application, and the receivable is the security in case of a buyer payment default.

Thus, making financing collateral & hassle-free.

Improves Cash Flow Cycle:

Asset-based financing speeds up a business’s cash flow while securing the extra cash needed to procure the asset. It is ideal for most companies facing poor cash flow.

Capital for Business Expansion:

It is the perfect short-term funding solution for businesses. Cash advanced can be used to pay employees and suppliers, or be invested in expansion and growth activities.

Accounts Receivable vs Accounts Payable

Unlock the comparison of receivables vs payables to gain a better conceptual understanding.

Drawbacks of Asset Finance and Asset-Based Lending

In the case of asset finance:

- It is a long-term financing solution as asset instalments are usually longer than 1 year

- Although payments are made in instalments, it may cost much more than using funds due to accruing interest

- In default on loan payments, the asset lender may seize the asset to recoup funds. This resolution could hurt the business’s performance or growth

In cases where the asset backs financing:

- The seller may be held liable in case the buyer defaults. It is not ideal for businesses with counterparts holding a greater likelihood of bad debt.

- The risk is greater with transactions involving riskier goods such as perishable or flammable items.

Nevertheless, the benefits outweigh the risks of asset-based lending as opposed to asset finance.

Asset finance holds greater risk as businesses are yet to realise the benefits of the asset. However, in the case of asset-based lending like invoice financing, commercial transaction has already happened.

Know the costs associated with invoice-based lending and learn how fintech companies like Velotrade make the process more convenient.

About the author

Velotrade Editorial

Official content from the Velotrade team.