Poor cash flow can kill a business, even a profitable one. To prevent their demise, SMEs need to identify the ‘leaks’ that drain their cash reserves.

One of these is late payments. SMEs and new businesses are especially vulnerable, as they typically don’t have large reserves of cash to cushion them, and have difficulty accessing traditional sources of funding.

In Asia Pacific, the average frequency of late B2B payments was 87.9 percent in 2018. While that’s a 1.3 percent drop from 2017, it’s still a high number based on D&B report. But even this high figure fails to portray the human and economic costs of late payments.

According to the Association of Chartered Certified Accountants (ACCA), micro and small businesses are less likely to increase capital expenditure or their workforce when faced with late payments. A multinational survey of SMEs reveals that late payments cause a gamut of undesirable effects, from reducing wages and future investments to eschewing Christmas bonuses.

While the onus should be on the customer to pay for the products and services they received, businesses can also implement strategies to speed up payments.

Update the Customer Master Database

Your customer master data should include information like payment terms, dollar limits on credit, discounts, and the like. This will allow you to quickly check what items or services a customer purchases and how much they can buy on credit.

The database will also reflect payment agreements, such as 50 percent payment on contract signing and the other half on delivery. It will show each customer’s payment history, giving you a view of who tends to pay on time and who tends to delay, and by how many days.

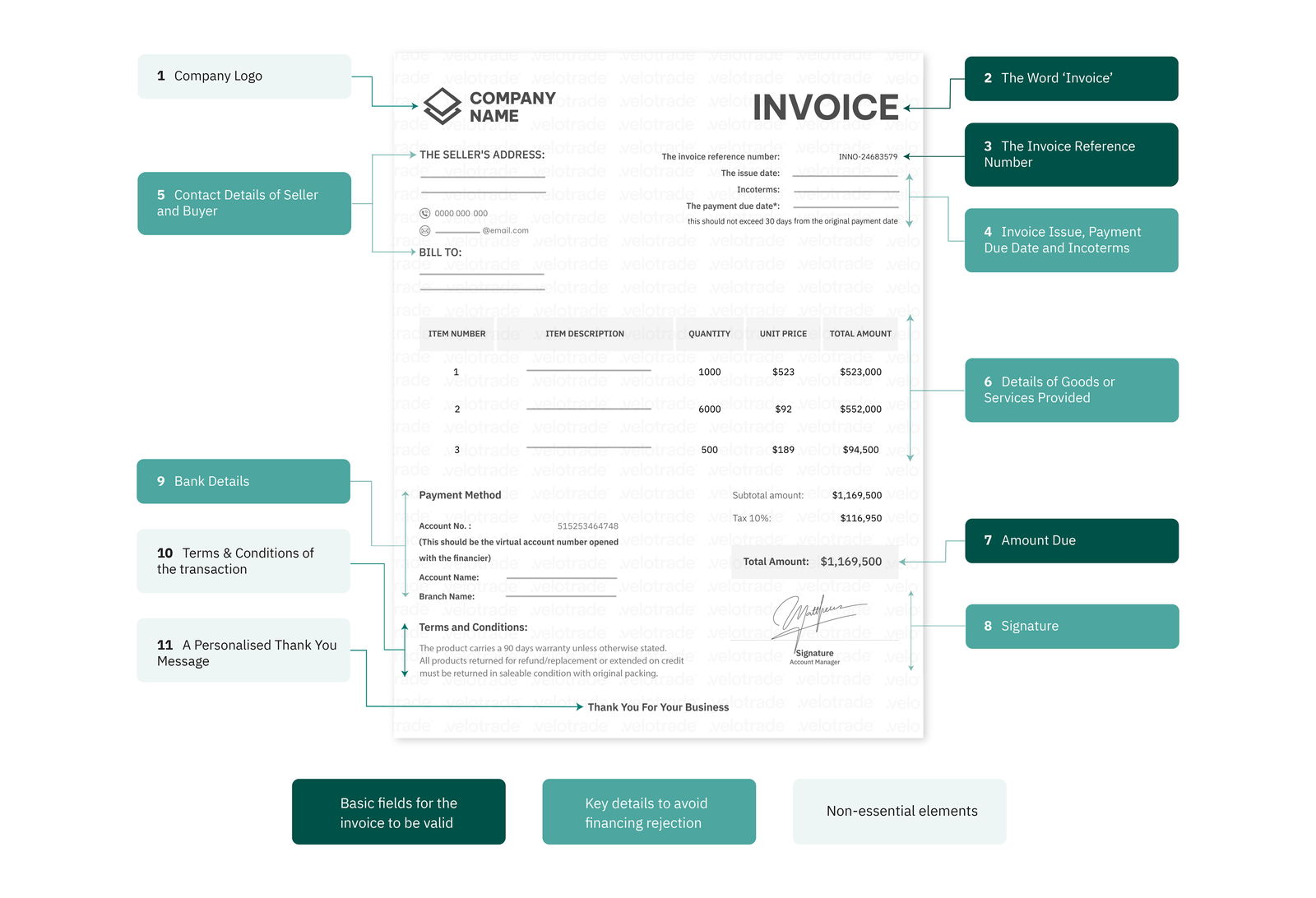

Apart from that, it’s important to include accurate and up-to-date data on the customer’s address, necessary information for the invoice, and the contact details of the persons who will receive the invoice and process the payment. This way, you’ll avoid payment delays related to inaccurate documents.

Moreover, tracking regular cash flow data helps firms be aware of their cash conversion cycle and avoid unnecessary expenses.

While a task like checking whether a company’s address is up-to-date or the recipient’s name is correctly spelled may seem trivial, the effort can come a long way. After all, ACCA notes that routine administrative delays, including those caused by errors, are among the most common reasons for late payments.

Brought to you by Velotrade, a marketplace for corporates to access financing.

Automate Invoicing

In a study of late payments in Asia Pacific, 68.2 percent of respondents said that e-invoicing led to quicker payments. By automating invoicing, you can reduce the occurrence of routine administrative delays and errors as it removes the need for manual data entry.

You can even automate follow-ups,no small advantage considering that five to 10 percent of all administrative work, equivalent to up to 20 days a year, is spent chasing payments.

With the myriad of affordable software solutions out there, it’s easy to begin automating your invoicing process.

For starters, check if the bookkeeping and accounting software your company uses has an e-invoicing feature. This will save you the time and cost of having to adopt a new tool. If it doesn’t have one, ask if such a feature is in the pipeline. You can also find out if the software is capable of integrating with other apps that may provide e-invoicing capabilities.

Keep in mind that it’s best to choose an e-invoicing solution that’s cloud-based so you can update and access your invoices on any device. Many cloud-based software also allow integration with third-party apps.

Besides, streamlining invoices and payment procedures, digitisation brings many benefits to businesses.

Get Real-time Updates

Using cloud-based tools, you can get a real-time update on your accounts, which means you’ll always have an overview of your company’s financial health. And with the launch of the Hong Kong Monetary Authority’s open API framework, you can expect more software to be capable of integrating with bank feeds.

These tools help automate the invoicing and accounting process by automatically reflecting customer payments on your books. This means you can see when a payment has come through. It also means you can see when a customer hasn’t paid, so you’ll know right away that you need to follow up.

Document Your Process

Have an internal manual for your invoicing and payment collection process. At first, these steps may seem obvious, but you’ll actually face plenty of decisions along the way.

These include:

- How many days you should wait before following up after sending the invoice

- How you should follow up: through email, messaging, phone, etc.

- What to do when a payment is more than 30 or 60 days late

- Who should follow up, and who should be copied in the email

As you see, these are steps that you’ll probably need to take every month,so decisions shouldn’t be a guessing game. Talk with your sales and accounting teams to set up a process that improves the speed of payment collection but also maintains a positive customer relationship.

It also helps to write email templates for routine and recurring scenarios,like sending an invoice, first follow-up, and so on,so you don’t waste time writing a message from scratch every time.

Invoice Financing with Trade Credit Insurance

Through invoice financing you will not only receive an advance payment and improve your short term liquidity situation, but on a case-by-case scenario, you also receive Trade Credit Insurance.

The Insurance will be useful of course in a customer default scenario but it will also help speed up payments when your customers intentionally delay settling their invoices.

There is often an asymmetry of bargaining power between Supplier and Debtor, especially when the Debtor is large, and the Supplier is not of strategic relevance to the Debtor.

After a specified payment delay the Trade Insurance Company will need to be notified. Debtors are seldom comfortable with the reporting as it will impact their credit standing with traditional financial institutions and are therefore likely to accelerate payments.

Customer Credit Approval Criteria

If you don’t have a clear, written policy on granting credit approval, it’s time to create one. It needs to set the requirements and procedures for qualifying customers for credit.

For instance, it should identify the circumstances that require you to do a credit history check on a new customer, such as when they intend to purchase large volumes of product on a regular basis. If you’re a small, fledgling business, your sales team may be tempted to simply accept such a customer without question, but it never hurts to find out how likely they are to pay.

Your policy also needs to provide a timeframe for approving or rejecting customer credit. By setting a strict time period, you don’t hamper sales and the potential client will know when to expect your decision.

Create an Accounts Receivable Ageing Report

Depending on the accounting software you use, you may or may not have to create an accounts receivable ageing report manually. This report shows you who hasn’t paid you and for how long. If you issue credit memos, you can also see which customers haven’t used them.

The key aspect of an ageing report is the date range. You can create 30-day time periods, as the example above shows, or break them down into shorter timeframes.

Over time, the ageing report will reflect how effective or ineffective your payment collection strategies have been. It will also help you identify potential bad debts.

And if you plan to take out a loan through invoice financing, you can use this report to show the financing company how much you expect to receive in customer payments. You can also use it to determine which invoices you can safely offer in exchange for cash.

Make a Customer Payment Plan

It’s easy to become suspicious of customers who don’t pay up, but the hard truth is that they may be experiencing cash problems. Perhaps their own customers haven’t paid them, constricting their cash flow and causing a domino effect on their suppliers.

In fact, bankruptcy is the main reason for uncollectible B2B payments in the Asia Pacific, especially in the business services, construction, consumer durables, and electronics sectors.

When you notice that a client has delayed payments for more than 30 or 60 days, or consistently pays late, find out what the problem is. It may be a case of administrative bottlenecks or understaffing on their end, or it may be serious cash flow problems.

Come up with a payment plan to help them out. This may include extending payment terms or encouraging early payments. The important thing is to have an honest conversation with your customer and maintaining the relationship.

Stay Vigilant

Economic volatility and political uncertainties may be blamed for bringing down businesses and industries, but late payments can also choke them. This is especially true for micro and small businesses.

Yet, SMEs are considered vital to Asian economies and need to thrive. In Hong Kong alone, they constitute 98.3 percent of the total business units and employ 45 percent of the total workforce.

As an SME, you need to protect your very lifeblood, cash flow, and work proactively to keep it moving and avoid clogs and leaks. Speeding up late payments is one major way to accomplish this and keep your business financially healthy.

About the author

Velotrade Editorial

Official content from the Velotrade team.